Can I retire? It’s probably the most exhilarating and anxiety-inducing question in all of personal finance.

To help answer it, you can work with a financial advisor, or punch your numbers into an online calculator that will simulate millions of possible market outcomes. And those calculations are important. I wouldn’t retire without them.

But even the best projections can’t answer the most personal part of the question: What does your money need to do to support the life you actually want? That’s where clarity about your spending—and the right tools to understand it—can change everything.

In this piece, you’ll hear from real YNABers who found that confidence in retirement doesn’t come from predicting the future. It comes from finally understanding their spending and using that clarity to make fearless decisions about what comes next.

Because there’s another number that’s just as important as how much you’ve saved or how your investments will perform. Without the right tool for the job, it’s nearly impossible to get an accurate read on this number.

Understanding it allowed YNAB customer CJ to say this:

In five years, I went from trapped in a stressful job due to debt and fear, to retiring fearlessly.

The number we’re talking about is, of course: How much do you spend?

Not “How much did you make at your final job before retirement?” Not “How much do you think you spend in an imaginary typical month?” Not “How much would you like to pretend you spend on dining out?”

We mean: How much do you spend when you’re living the life you actually want?

CJ’s story is a perfect example of how understanding your spending creates freedom, not limitation. And she’s not alone. Many YNABers have found that when they finally saw what they actually spent (and what mattered most), confidence followed naturally.

Another YNABer, Poshi, wrote in with a relatable roller coaster: years of worrying about whether they would have enough money in retirement.

I was so unhappy at my job—a job I used to love, but had changed so drastically for a number of reasons. Also, my wife needed more support from me than I could give while also working full-time. With all that said, I was financially terrified at the idea of retiring. I had been using YNAB for over a year, and was able to run reports to see how much money we really needed for our budget if my salary went away—especially if I wasn’t ready to start taking Social Security payments.

While our financial advisor could run all kinds of scenarios for us, without YNAB we would not have been able to tell what our budget needs really were. I was able to retire in March, 2023—much, much sooner than I ever had thought. Since March, YNAB has helped me ensure that we stay on track and that I won’t have to go back to work!

When Poshi says, “We would not have been able to tell what our budget needs really were,” they mean:

- Without a spending plan, you can’t come up with realistic average monthly or annual spending.

- Without a spending plan, money slips through your fingers and it’s hard to even say where it went.

- Without a spending plan, your mind fills up with “what-ifs?” that make you feel scared and uncertain, but with no actual way to explore what you would do if the “what-if” showed up.

Once you know what you truly spend, the next challenge is preparing for all the unknowns that come with retirement. Because no matter how perfect your plan feels today, change is certain.

Curve balls are inevitable

One fear that keeps us from retiring is, “What if I have enough money to cover my expenses now, but not in the future?” It’s a constant hum of money worry. What if medical or housing costs go up? What if my partner passes away first? What about inflation?

A spending plan lets you explore these situations and see how you would respond. These are not groundless fears, of course! They’re questions you have to wrestle with. And they’re questions about spending: “If this happens, how will I change my spending to deal with it?” Without a spending plan, you can’t answer that question; you can only get dragged down by worst-case scenarios.

For Taia, those same principles—clarity, flexibility, and intention—became essential tools during one of the hardest transitions imaginable.

My husband was a wonderful provider and lead in the money management. He worked and paid the bills. Our only debt was the mortgage. He was primary on all accounts. Then he died very suddenly, leaving me to raise our kids and sink or swim, filling his big shoes. I was cut off of all credit cards as he was the primary and my stable income quickly changed to an unknown status. I had funeral bills, medical bills, and lawyer bills, all unforeseen. Life was grieved, scary, and unstable from moment to moment.

My sister had recommended YNAB for years. But 9 months of widowhood and realizing I don’t know what’s going in or coming out, I decided to give YNAB a try. I loved it! Over the next year, I’ve tracked my spending and adjusted where needed… truly transitioned into YNABing. I am confident that I know what’s coming in and going out. I plan for what’s to come and have significantly decreased my anxiety over my finances. I know that I have a plan and it’s sustainable. I can focus on my biggest priorities: my children.

Retirement isn’t a season of stability. But no part of life is! The tools that help you weather unpleasant financial surprises during your career don’t stop working just because you retire.

A good spending plan is flexible. You make a plan for the situation you’re in now, and then when the situation changes, you change the plan. That goes for big changes and small ones, and the habits you learn while navigating small changes from day to day will be useful when life throws curve balls your way, too.

Tips for getting ready to make the leap into retirement

These stories show what’s possible when you have clarity and confidence about your spending. But how do you get there? If retirement is on your horizon—or even just a distant dream—here’s how to start building that same confidence today.

Say you’re already using YNAB, or thinking about signing up for a 34-day free trial. How do you actually use it to prepare for retirement or figure out whether you’re ready?

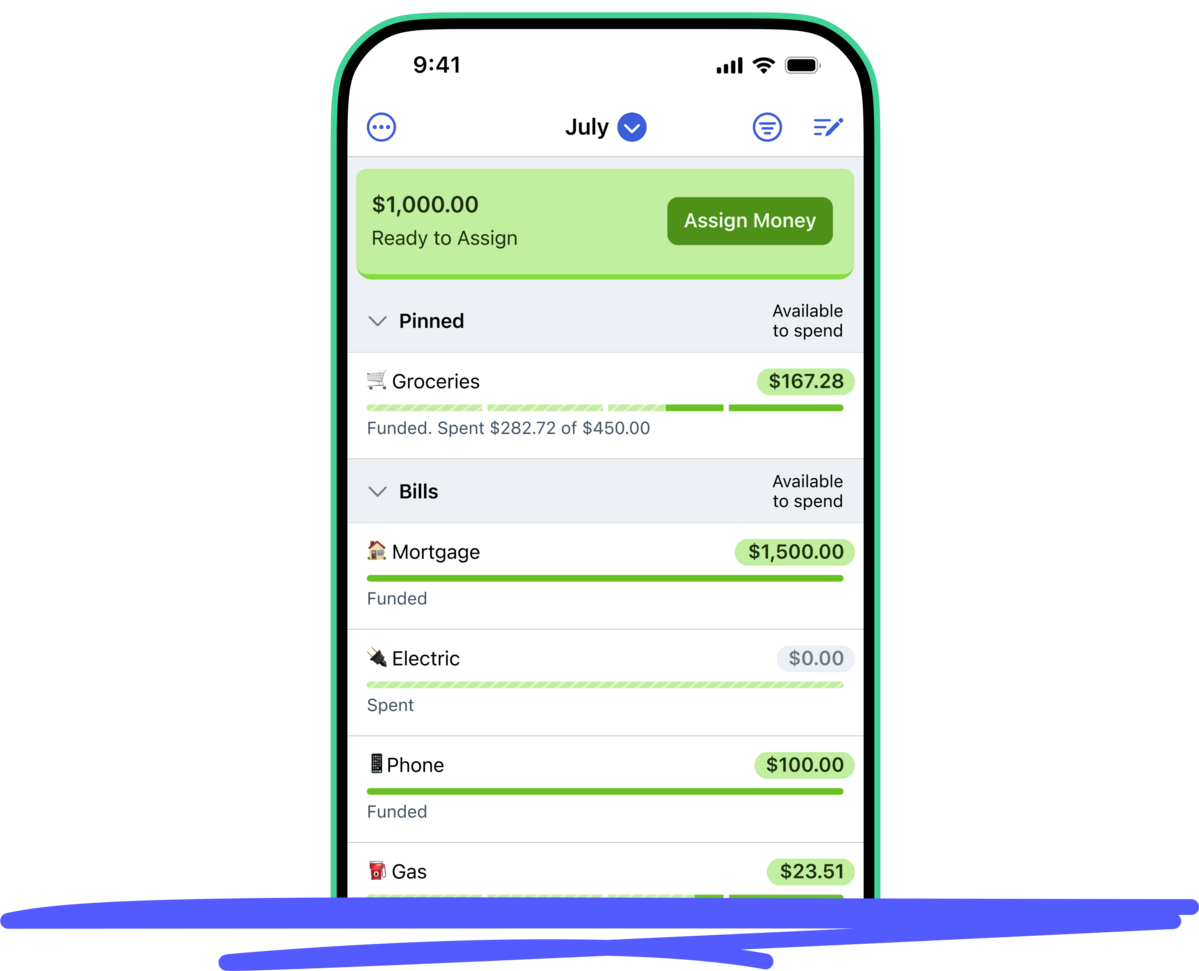

- Build your buffer. The YNAB Method teaches you to get a month ahead. That means you’re fully funded on the first of the month with money you earned last month or earlier. Of course, retiring means you’ll have savings that will take you months and years into the future, but if you’re not already fully funded on the first, you’re not ready to retire.

- Do a “retirement rehearsal.” If you’re planning to change your spending in retirement, simulate that now. Use YNAB to practice living on your projected retirement income for 3 to 6 months before actually retiring. Think of it as a dress rehearsal.

- Ask yourself YNAB’s five questions to help align your spending with your priorities—but especially the Stability and Flexibility questions.

The Stability question is: “What larger, less frequent spending do I need to prepare for?” The Flexibility question is: “What changes do I need to make, if any?” Together, these two questions allow you to peer into the future in a productive way that helps you be emotionally and financially ready for the unexpected.

- Use your retirement calculator and your spending plan in a complementary way. Your retirement calculator takes your sources of income in retirement—savings, Social Security, pension, etc—and tells you how much you can safely spend monthly or annually. Your spending plan tells what you can actually buy with that amount of spending money, and you can decide whether that fits the lifestyle you want in retirement.

- Accept that there are always unknowns. One fear that keeps people from retiring is, “What if all of the worst-case scenarios showed up at once?” When you’re talking about one of life’s biggest transitions, this is a natural thing to worry about, and no one can prove that it won’t happen.

However, think about all of the decisions you’ve made in life so far that weren’t based on avoiding a worst-case scenario. If you lived life this way, you would never really live at all.

I’m not advising anyone to take an uninformed leap into retirement. But the best you’ll ever be able to say after crunching all the numbers is: I think this will probably work out, and when problems come up, I have the right tools to make decisions about how to weather them.

In other words, you don’t need retirement certainty to have retirement confidence. Confidence doesn’t require being able to predict the future—nobody can do that. It just requires clarity and flexibility, and that’s what a spending plan is all about: spending joyfully without second-guessing, and being ready for change.

(1).png)

As she works toward retirement, music teacher Pamela is feeling more confident day by day.

I spent most of my adult life, including two marriages, handling money on a wish and a prayer. Now my money does exactly what I tell it to do. I’m still learning—I still listen diligently to Jesse’s podcast, Ben and Ernie’s podcast, and catch Hannah’s videos whenever I can. I recommend YNAB to anyone I hear struggling with money.

You’ll never predict the future—but you can make a plan for the life you want. Get YNAB, get good with money, and retire with confidence.

Good With Money: Another Real YNABer Retires Fearlessly

Get inspired by Donna L., a real YNABer who retired without money worry. “The day I told my coworkers I was retiring, many of them asked me how. My truthful answer was YNAB.”

YNAB has enabled me to know exactly how much I needed and plan for, and gave me the ability to retire early with confidence. I am not wealthy so anyone can do it. Looking at my checking balance and knowing my entire adult life prior to YNAB I relied on overdraft and credit card float astonishes me how much I learned with YNAB. My big win was through YNAB, I stopped relying on overdraft. I plan my immediate and true expenses with Rule #1. Every dollar has a job.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by budgetbuddy.

Publisher: Source link

Publisher: Source link