As I type this, I’m jumping through the various hoops involved in buying a 2023 Tesla Model Y, a spectacularly expensive, large luxury “crossover” that is absolutely loaded to the gills with excess: all wheel drive, faster acceleration than a Lamborghini, enough space for seven people and enough computer gadgetry to function as a small Google data center.

Update: Looking for the ongoing tracker page? It’s here at “The Model Y Experiment“

The total net cost of this thing to me after all the taxes and tax credits* will be about $52,000, which is just a stunning amount higher than the Honda van it is replacing. That old classic cost me $4500 when I bought it off of Craigslist twelve years ago, and it had served me dutifully until just last month, crisscrossing the mountains and deserts of this country and also helping to rebuild a considerable swath of houses in my neighborhood.

I’m supposed to be a frugality-oriented financial blogger, and I’m also known for hating car culture – I think most people use cars about ten times more often than they need to, and most people drive cars they can’t afford. So why the hell am I buying a new one?

From those first three paragraphs, you can see I’m feeling plenty of self-mockery and ridicule over this new purchase. If you’re also a naturally frugal person, you can surely relate to the thoughts and you probably also agree with me that I’m off my rocker.

And indeed, I’m still on-board with frugality and healthy self mockery. After all, it was this overall life philosophy that earned me an early retirement 18 years ago, which provides all of the glorious freedom I enjoy now.

It was also the philosophy that allowed me to procrastinate on buying this expensive car for the last four years, even as countless people both close to me and out on the Internet egged me on and told me I should just loosen up and treat myself.

But there’s a classic slogan that applies to many areas of life, and it is something I like to dig up and ponder every now and then:

“What got you here,

Won’t get you where you’re going.”

How does that piece of wisdom apply to frugal living and enjoying a long life of early retirement?

A quick story from a recent run to the grocery store will explain:

I was standing there in the bakery aisle, hoping to restock with a loaf of Dave’s Killer Bread for the next day’s breakfast with some visiting friends. But since this was in a standard grocery store rather than the Costco where I usually shop, the damned stuff was priced at an eye-watering $6.99 per loaf (instead the $4.50 or so I’m accustomed to paying, and even at the bulk store this stuff is about double the price of normal bread).

“DAMN YOU KING SOOPER’S!”

Was my first response.

“WHO THE HELL DO YOU THINK YOU ARE, TRYING TO SELL BREAD FOR SEVEN BUCKS!!!”

Then I went through a whole mental battle of what I call Grocery Shopping With Your Middle Finger:

“Should I just boycott this bullshit?”

“Hmm I wonder if any of the other competing brands are any good?”

“What else is a good substitute for bread for this breakfast?”

And then thankfully, after exhausting all other mental options, I settled on the correct one:

“JUST BUY THE BREAD YOU DUMBASS!”

“Because you are never going to wake up in the future and look at your bank account and think, shit, if only I had an extra $2.49 in there I would be a happier person.”

That night, I came home from the store and shared this funny tale with one of my guests. He understood perfectly because he too had earned his own retirement through a lifetime of grinding in tough jobs and disciplined frugality. And despite the fact that he has a net worth several times higher than mine, he admitted that he faces exactly the same mental battles over splurging on himself.

This same friend gives freely to charitable causes, has supported a local school for decades, and is always the first one to pull out the checkbook if a friend has hit hard times or is looking for a trusted business investor.

But he still has trouble bringing himself to take an Uber to the airport instead of riding the bus which takes an hour longer.

We both realized that we were being too cheap with ourselves, and we needed to work on it. And we came up with a set of three ideas that should hopefully work together to help us have more fun with our life savings, while we are still alive:

- the Minimum Spending Budget,

- the Dedicated Money Wasting Account,

- and the Splurge Accountability Buddy.

Principle #1: The Minimum Spending Budget:

Suppose you’ve done well over the years and amassed a pile of productive investments worth about two million dollars. Yes, this is a lot of money for most people, and that is the point: this hypothetical person truly has it made.

But as it turns out, most Mustachians I know with this level of wealth are still living very efficient lives, usually with a spending level of under $40,000 per year. On top of that, they typically live in a mortgage-free house and still have various forms of side income from a small business or two.

The 4% rule tells us that this person should be fairly safe spending up to about $80,000 per year from that cozy nest egg, even if they never earn any other money.

If this person wanted to be ridiculously conservative and set the spending rate at 3%, that still leaves about $60,000 of fun money every single year.. Plus, again, any side income, future inheritances, and social security income only add to the surplus.

Thus, a reasonable minimum spending level for this person might be $60,000 per year.

And in most cases, they know this, but still go right on living on $40k or less and claim they have everything they could ever want.

But if you watch carefully you’ll still catch them firing up the middle finger at things like $6.99 Dave’s bread or the $14.00 Cabernet at the restaurant or driving around in a gas guzzler even when they would prefer to have a proper, modern electric car.

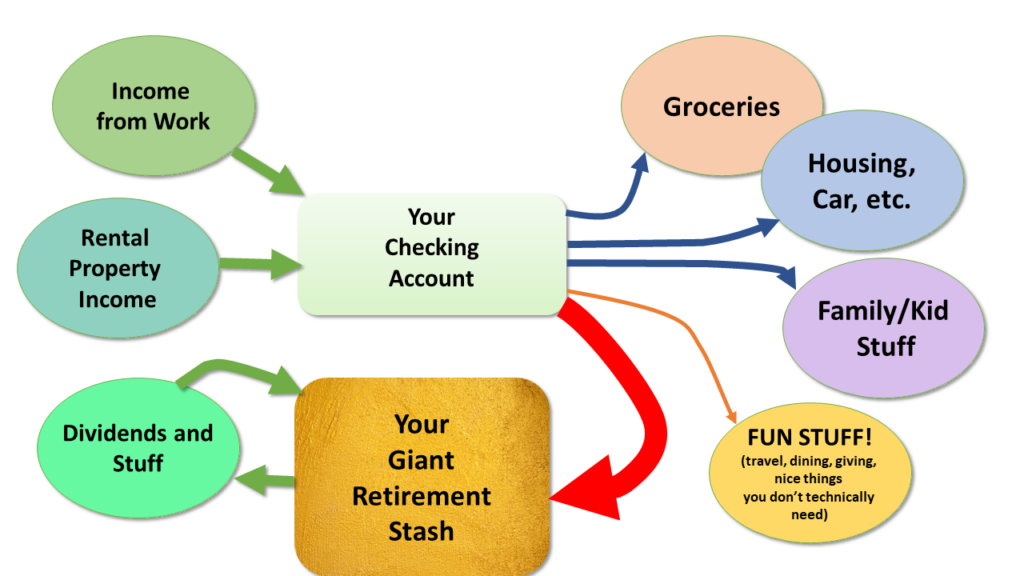

And whenever these people do get extra money, their first instinct is to stash it away on top of the already-too-big pile. In diagram form, their money flow looks like this:

Note that while this person is great at accumulating money through that big red arrow firing money back into the ‘stash, their “fun stuff” arrow appears quite flaccid and withered.

Which is a perfect segue to ….

Principle #2 – the Dedicated Money Wasting Account

Lifelong habits are hard to break, and it’s sometimes hard to “waste” your own hard-earned money on things that seem frivolous, even when you know intellectually that you have way more money than you’ll ever spend.

But have you ever noticed that if you are spending somebody else’s money, preferably an anonymous corporation, it feels different?

For example, when you’re on a business trip and you just show up at the dining table to eat and drink and you never see the bill, you probably don’t fret about the prices, right?

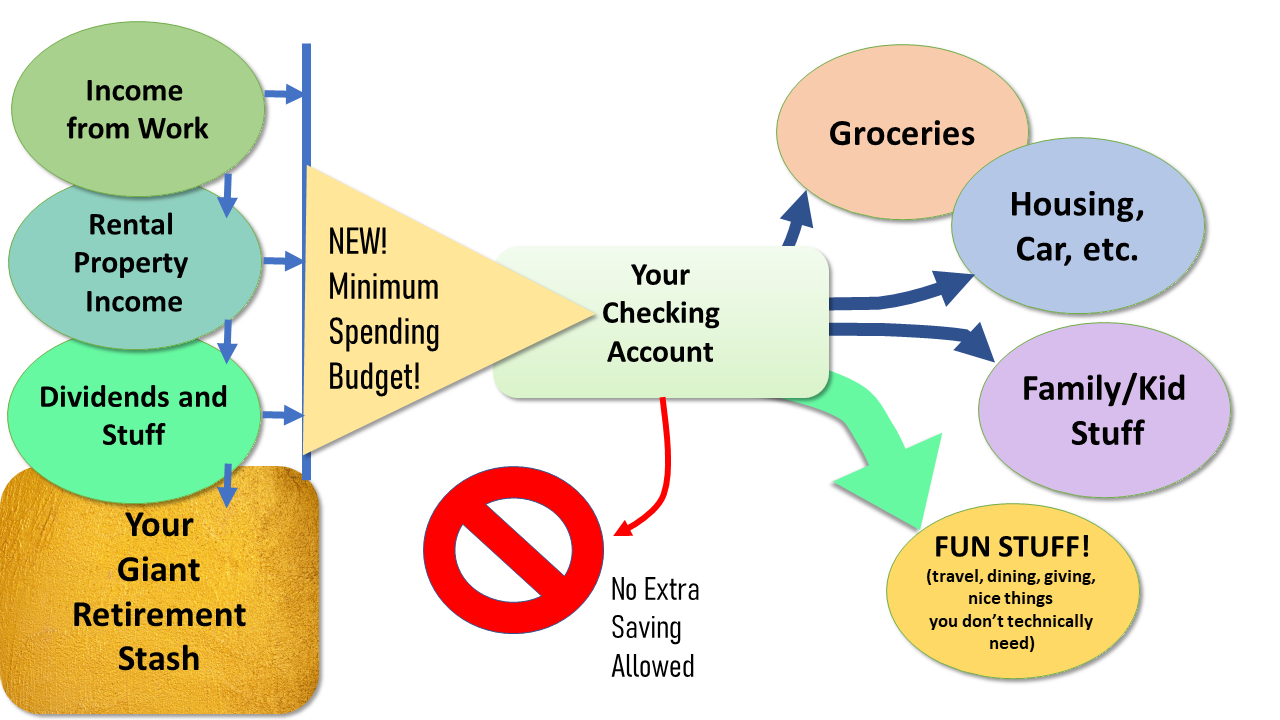

The key is to make your own money feel like somebody else’s, and you can do it like this:

- Re-brand your main bank account – henceforth it is the FREE FUN MONEY account.

- Set up an auto-deposit of your minimum spending budget that drops in each month (if you suspect that you might currently be too frugal, make this at least $1000 per month higher than your current spending level)

- The only way you are allowed to use the money in this new account is to spend it on anything and everything, or give it away. It can be used for both necessities like groceries and your utility bill, but also your luxuries like travel and dining and generosity.

But the key rule is this: You are not allowed to follow your old habit of sweeping out the surplus each month to buy more and more index funds as you’ve been doing your whole life.

If the free fun money starts building up, which it probably will because you are way out of spending practice, it will stare you in the face and tell you to do a better job.

And this can and should be FUN! Now you can get the best organic groceries even when the price seems exorbitant. Go out for dinner or order delivery whenever you like. Surprise your loved ones with concert tickets, join your friends on snowboarding or beach trips, or even pay for an entire group vacation, allowing people to go who couldn’t normally afford it so easily.

- Technical Note: Some people have income or wealth levels are so high that it would be insane to spend at a 3% rate. For example, a $10M fortune would lead to a $25,000 monthly spending rate, which is obviously ridiculous.

In this situation, you can still leave your dividends reinvesting but still give yourself a bigger, no-saving-allowed budget to get some practice being more relaxed and generous. The real point here is to just stop sweating the details so you can have more fun.

Principle #3 – The Splurge Accountability Buddy

Many of us frugal people tend to stick together. And most of us have different versions of the same problem: we know logically that money is plentiful these days, but our emotions keep us stuck in our old ways of optimizing too much.

But I find that when I team up with local friends who are actually trying to battle these same habits, we can question each other’s decisions, call out cheapness when we see it, and cheer on splurges when we know the other guy would enjoy it.

My super wealthy friend from above has become much better about treating himself (and his family) to quality goods for the home, amazing trips together, and just a general reduction in his stress over being “efficient with money”

My friend and HQ co-owner Carl (Mr. 1500 Days) has finally replaced his beaten-down minivan with a spiffy new Chevrolet Bolt electric car, and is loving that leap into the future.

And of course Mr. Money Mustache, after squeezing one final mountain road trip out of his 23-year-old Honda van, is finally allowing himself to get the Tesla he has been talking about for half a decade.

A recent life change (becoming a co-owner of a fixer-upper vacation rental compound in beautiful Salida Colorado) has reignited the travel fire in my heart and made me realize how much I do love getting out to distant places for visiting, mountain biking, gathering with groups of friends and my favorite activity of all: Carpentourism.

Running the Numbers: how ridiculously expensive is this car?

This is the perfect start to my experiment in spending more. Realistically, a $50,000 car is going to cost me about $10,000 more per year than my old van was burning. With the biggest costs being these:

- Foregoing roughly 8% annual investment returns on the 50 grand: $4000

- Depreciation on the car: an average of $3000 per year over the first 10 years

- Higher insurance premiums: $1000 more per year

- Replacing those exorbitantly huge performance tires when they wear out, and probably things like repairing the all-glass roof someday when it meets Colorado’s pebble-strewn mountain roads: the remaining $2000 or so.

Since I personally had a spending deficit of several times more than $10k per year, I figure this is a solid first step. And, since the car’s primary purpose is things like epic camping trips, dream dates, and long adventures around the country, it will definitely help me spend more on experiences, hotels, and go out to dinner a bit more often as well.

“This Privileged Rich Folk Talk is Making Me Sick, why don’t you give your money away to charity, or to me?”

In general, I agree: the world has problems and the richer you are, the more you should consider giving generously.

But also, to be honest, the whiny people who constantly send complaints like this out to strangers on the Internet really need to get a life. It’s great to encourage philanthropy through positive examples, but completely unproductive to send negativity to shame people you don’t even know for not following your own personal value system. The world has seen more than enough of this.

On top of that, this one-sided thinking can be counterproductive. Both of my friends have given generously throughout their lifetimes. In my own case, I have donated over $500,000 to the best causes I could find during the years I’ve been writing this blog, but I was still refusing to let myself replace that 23-year-old van.

And that overthinking was leading to even more of a scarcity mentality, as I compared my own meager spending to these bigger numbers of my donations, and found myself thinking things like,

“Damn, I’m spending $100 on this dinner date which sounds like a lot, but I also spent ONE THOUSAND TIMES more on donations last year, which sounds like even more. Maybe I am spending too much and need to cut back on EVERYTHING!”

And then the fear side of my brain would illogically chime in: “Yeah and you’re going to make us run out of money and be poor forever! waaaah waaaah! Cut back and optimize and conserve!”

I think there is a happy medium here.

Yes – be a super, duper responsible steward of your life savings.

And yes, give generously with all your heart to charity.

But yes, it’s also okay to set aside a portion of the money you’ve earned, for frivolous spending on yourself and those closest to you. You’re not a bad person for having a few nice things.

It’s okay to pay that extra hundred bucks to sit a bit closer to the front of the airplane instead of the back if it helps you enjoy your vacation and spend a joyful half hour walking FREE at your destination while the 49 rows of people behind you fuss infuriatingly with their shit in the overhead bins.

It’s okay to buy the frozen berries at Whole Foods even though they cost eight times more than Costco charges, if it spares you from making a second unpleasant trip through parking lot hell.

And as for me, I am calling it okay to, at last, double flip the Autopilot stalk in my new Tesla and lean back as it it shoots me gracefully through even the highest mountain passes, forever leaving the desperately underpowered wheezing and gear shifting and noise* of the gasoline era behind, forever.

Rest in Peace, Vanna – 1999-2023

—– Bonus details and links —-

* How to get rid of an old vehicle:

I ended up using an online car salvage service called Peddle*, at the recommendation of a friend. With about five minutes of entering the details of my old Honda, their system offered me $715, and then a towtruck came and took it the next day – and actually gave me the payment in cash, which I found kind of fun. I made a point of using all of that money for splurges like dinners out, in keeping with the theme of this article.

* I later signed this blog up for Peddle’s affiliate program so that link will benefit MMM if you use it.

* A useful tip for more effective splurging:

Try to find the truly negative aspects of your life and focus any additional spending on improving those things. But it’s a subtle art so you have to get it right if you want lasting results in happiness.

You don’t want to just reduce hardship or challenge like hiring someone to take care of every aspect of your house, because overcoming daily hardships and having significant accomplishments provides the very core of our life satisfaction.

You also don’t want to just upgrade the things that are already good in your life. For example, a friend of mine is a gourmet coffee expert, and he suggested that I upgrade my setup at home to include on-the-spot roasting, and fancy grinding and brewing equipment. But I already love the good quality coffee I buy off the shelf from Costco, so it would be counterproductive to invest time or money into changing this part of my life.

But when you have something that causes you regular angst and stress, whether it’s a leaky roof that makes you dread rain, or a long commute that makes you dread the daily traffic jam, or a body that is giving you trouble due to not being in the best of shape – those types of things are probably a good target for improvement.

In the case of my car situation, I had a Nissan Leaf which is wonderful to drive, but doesn’t have the range to travel anywhere outside of the Denver metro area. Then I had the van which is a clunky beast to drive, but is otherwise an amazing road tripper because I could bring along whatever and whoever I wanted. But the van was getting increasingly unreliable in several hard-to-fix ways which was making me nervous every time I thought about long distance travel. Which was causing me to avoid certain trips and miss positive lifetime experiences.

In other words, my lack of a reliable long-range car was a small but consistent source of negative stress.

Finally, Vanna gave me the gift of a final hot and smelly transmission failure on a mountain pass on the way home from my new project in Salida. It was just the nudge that I needed. And now I already feel excitement rather than dread at the prospect of all the road trips in the coming decades!

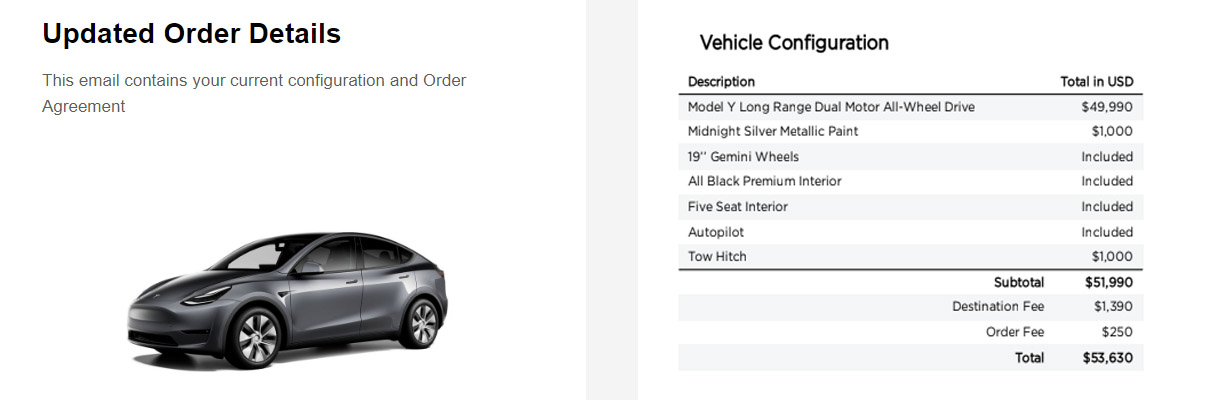

* Total cost of this Tesla:

- Model Y plus options and Tesla fees: $53,630

- Subtract $7500 federal EV tax credit

- Subtract $2000 Colorado EV tax credit

- (Note: this is equivalent to a $44,150 list price if you are cross shopping with other cars)

- Add back in $4674 of sales tax

- Add in first 3 years of Colorado new-car registration fees: $3000

- Net cost: about $52,000

Referral program: after I wrote this post, Tesla has re-started their referral program. So if you do happen to be in the market for any of the company’s products, we can both benefit from a small discount or some free supercharging miles or whatever if you use this code:- and thanks if you do!

New Tracker Page!

To go along with this article, I started a new page called “The Model Y Experiment” where I can share ongoing findings and Q&A about the ownership experience. I’ve driven and rented Teslas quite a bit in the past, so most of it will be pretty familiar. But as an owner I’ll get to verify the reliability and the quality of customer service, as well as any quirks and modifications and upgrades I do.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by budgetbuddy.

Publisher: Source link

Publisher: Source link