Do you wish you were better with money? You are not alone.

Most of us were never really taught how to handle money beyond “create a budget” and “save for emergencies,” and those leave a lot of gaps. What if there were a handful of habits that didn’t just plug those gaps, but actually reshaped the way you experience money?

What if the stress and all the late-night money worries could be replaced with calm, clarity, and even excitement about the future?

On a recent episode of Budget Nerds, Ben and I unpacked seven big shifts that transformed how we handle money. These aren’t tiny tips or one-off hacks. These are habits that unlocked lasting clarity and confidence—the kind that changed everything for both of us.

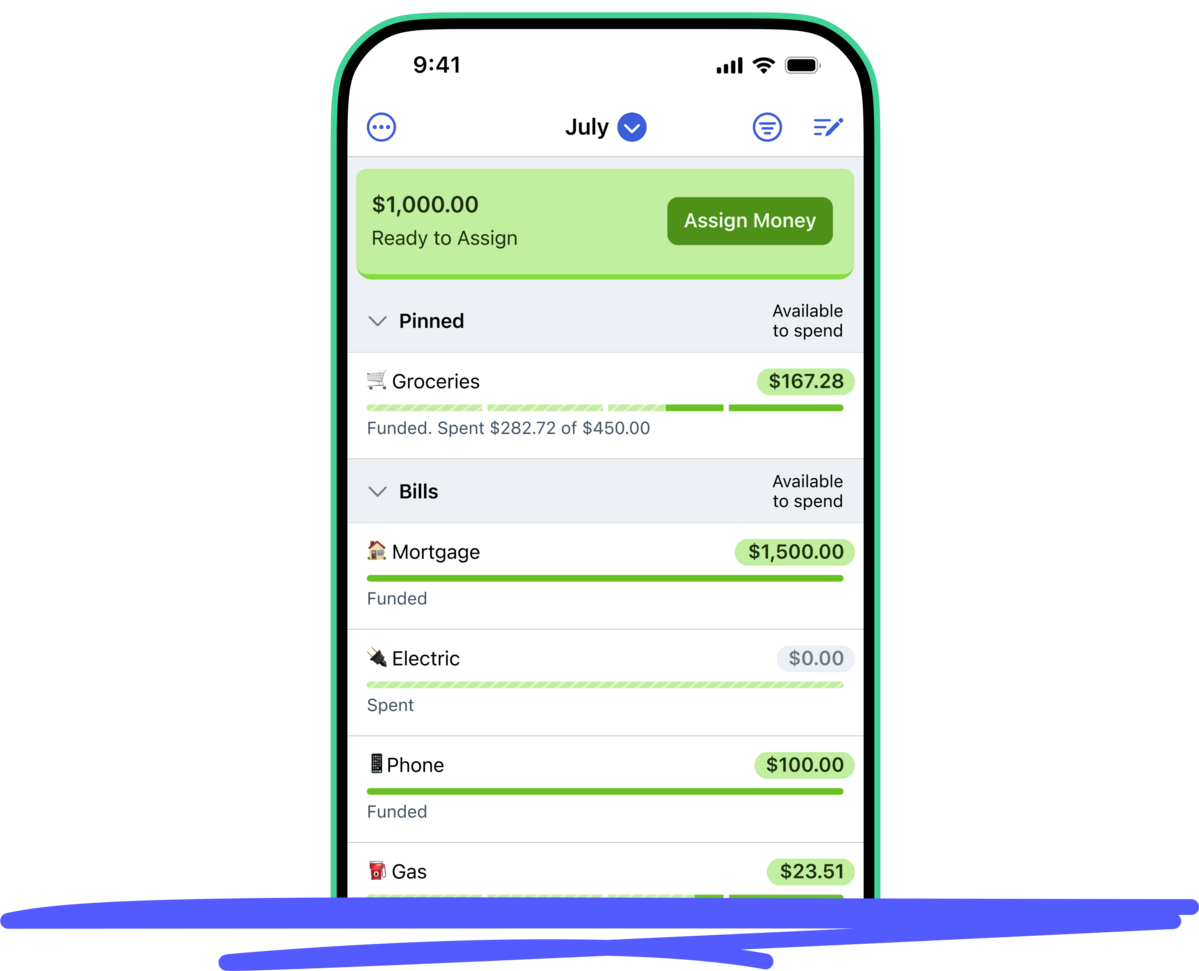

1. Give Every Dollar a Job

What it means: I decide what all of my money will do before I spend a penny of it based on what’s important to me. Some of my dollars will pay the mortgage, others will buy groceries, and I definitely need to set some aside for a round of golf here and there.

Why it works: Giving every dollar a job separates emotional decision-making from the moment of spending. I make trade-offs when I’m calm, not when I’m hungry at the grocery store. Later, I get to enjoy spending guilt-free, without second-guessing.

Try this: Open your bank app and see how much you have in your checking account. Now assign every one of those precious dollars a job—tell that money exactly what it needs to do! Notice how much clarity you have now and see if you’re more confident spending that money.

2. Work Only With the Money You Have

What it means: Instead of planning with money I expect to come in, like that paycheck next Friday, I only use what’s actually sitting in my account.

Why it works: Working only with money I already have forces me to face reality and acknowledge scarcity. I only have so much right now, and those dollars can only do so much. That limitation is powerful—it pushes me to prioritize, make trade-offs with open eyes, and be more intentional. And when I only use the money I have on hand, I can trust my plan. I know that each and every dollar in the plan actually exists in my bank account.

Try this: Go back to the plan you built in Habit One and see if this habit changes the jobs of any of your dollars. Is there something else you’d rather prioritize between now and the next time you’re paid?

.png)

3. Save for Non-Monthlies

What it means: Non-monthly expenses are all the things you don’t pay for every month—things like car repairs, holiday gifts, or my annual Costco membership. I treat these irregular expenses like monthly bills. I figure out the total amount I need, divide by 12, set aside that amount each month, and, BOOM!, the money is there when those things finally pop up.

Why it works: Saving for non-monthlies means there are no more nasty surprises. Those so-called “emergencies” stop being emergencies because I’ve already prepared for them. I don’t have to swipe a credit card and then figure out how to pay it off later, nor do I have to pull from savings and use money that was intended for something else. Instead, the money is sitting there, waiting, and ready to go. Once I started doing this every month, I honestly slept way better at night.

Try this: Pick one irregular expense (like annual subscriptions or holiday spending). Divide the total you need by 12 and start setting that amount aside every month. Then be sure to pay close attention to just how good it feels when you spend that money.

4. Get a Month Ahead (Live on Last Month’s Income)

What it means: Getting a month ahead means your spending plan for next month is completely funded (with real money!) before the new month starts. This month I’m spending dollars I earned last month, and then all of my paychecks this month will fund next month’s spending plan.

Why it works: Being a month ahead gives me breathing room. It frees up mental energy because I’m no longer obsessed with timing bills to my paychecks. Instead of bills waiting around for money, I have money waiting for bills. Ben went as far as describing a month ahead as “spiritual.” Okay, that may be a little dramatic, but I think I agree! Being a month ahead of your expenses feels like breathing room for the soul.

Try this: Pick one bill next month and try to have money set aside for it before next month begins. Once you taste that freedom, you’ll be motivated to keep going until all your expenses are covered. Fully funded on the first, babay!

5. Find the Money First

What it means: Before spending, I check if the money is there for that particular category. Do I actually have money set aside for this spending? If I don’t, I simply move money from another category—or decide the purchase isn’t worth it.

Why it works: This prevents overspending and forces me to weigh trade-offs in real time. It’s not “No, you can’t spend.” It’s “Yes, and here’s where it comes from.” I already know I can’t have it all, but finding the money first helps me prioritize what I want most.

Try this: Before your next discretionary purchase, first check to see if you have money set aside for the purchase. If there isn’t enough, what are you willing to give up to buy this?

6. Hold On to Cash Longer

What it means: Cash gives you options. Think of it like buying yourself time and flexibility. With cash in hand, you can choose whether to pay down debt, handle an unexpected car repair, or jump on a surprise opportunity without scrambling.

Why it works: It took me a long time to realize this, but holding onto cash—even for a few weeks—reduces my stress and gives me resilience. Sure, it’d feel great to pay off my debt faster, but when I hold onto a little extra, cash emergencies don’t derail me any longer, and I still pay down debt on schedule. The flexibility is worth far more than the small amount of interest I might pay.

Try this: Instead of sending an extra debt payment right away, set the money aside for 30 days. See how it feels to have that cushion available before sending it off.

7. Change Your Plan—Anytime

What it means: My circumstances and priorities are changing all the time and so should my plan. If I need more money for groceries this month, I move money from a less-important category. No shame, no guilt. I just change my plan and move on with life.

Why it works: Old-school thinking says changing the plan means you failed. YNAB taught me that changing the plan means I’m paying attention and being intentional. It’s proof my money is aligned with who I am today—not who I was three weeks ago.

Try this: The next time you overspend in one area, cover it with money from somewhere else. And do it guilt free! Notice how much better it feels to adjust the plan instead of feeling like you’ve blown it.

Start with One Habit

Don’t stack all seven today, I beg you! Pick one that you have the most energy around—maybe saving for non-monthlies or changing your plan—and try it for a month. It won’t take long before the habit locks in and you feel the difference. Then try one or two more. Before you know it, you’ll wake up one day and realize, “Wow, I’m good with money now!”

Tired of worrying about money? Sign up for YNAB, get good with money, and never worry about money again.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by budgetbuddy.

Publisher: Source link

Publisher: Source link